Non-ferrous

Non-ferrous

Base Metals

Rare Earth

Scrap Metals

Minor Metals

Precious Metals

New Energy

Price CenterDatabaseProReportsEventsCar Insight

Language:

Language:

SMM reported on July 8:

Regarding aluminum prices, the center of aluminum prices continued to move upward in June. By June 30, the most-traded SHFE aluminum 2508 contract closed at 20,580 yuan/mt. In terms of spot aluminum, the SMM A00 price on June 30 rose by 490 yuan/mt from the previous month-end to 20,780 yuan/mt. The average spot price of SMM aluminum in June (calendar month) was recorded at 20,535 yuan/mt, up 2.0% MoM from the previous month.

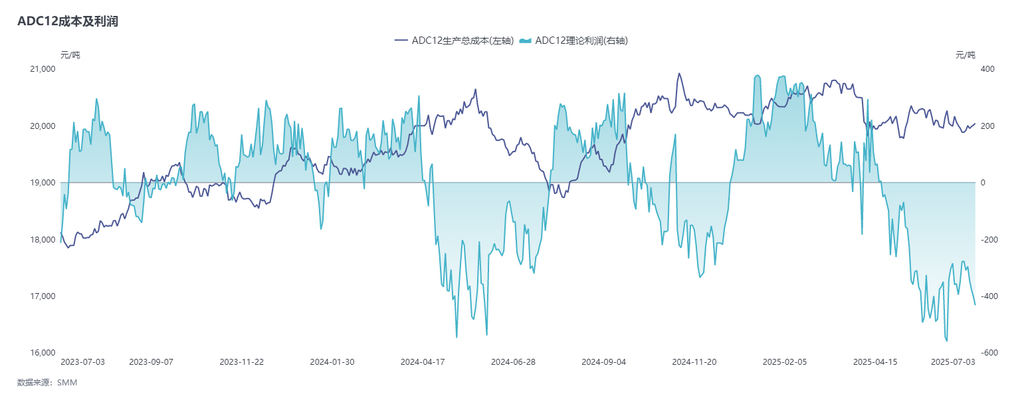

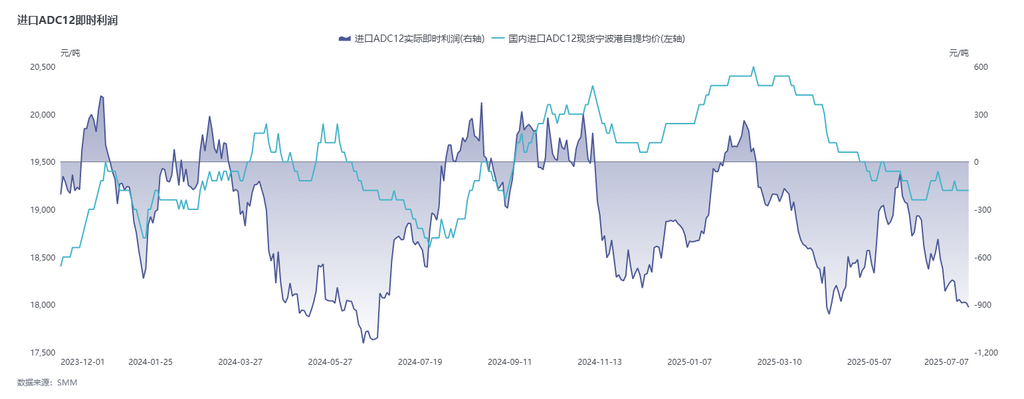

Regarding secondary aluminum alloy prices, on June 10, cast aluminum alloy futures were officially listed for trading on the SHFE. With a listing benchmark price of 18,365 yuan/mt, which was significantly lower than the spot price, driven by the need to repair the spot-futures price spread, the main futures contract opened strongly and surged to around 19,500 yuan/mt. Subsequently, the futures market basically followed the fluctuations of SHFE aluminum. By July 7, the most-traded cast aluminum alloy 2511 contract closed at 19,750 yuan/mt. However, the spot price showed weak upward momentum. On July 7, the SMM ADC12 price remained stable at 20,000 yuan/mt compared to the beginning of the previous month, and the theoretical premium against the main contract narrowed from 685 yuan/mt on the listing day to around 260 yuan/mt.

The following chart shows the price trends and price differences of A00 and ADC12 in recent years:

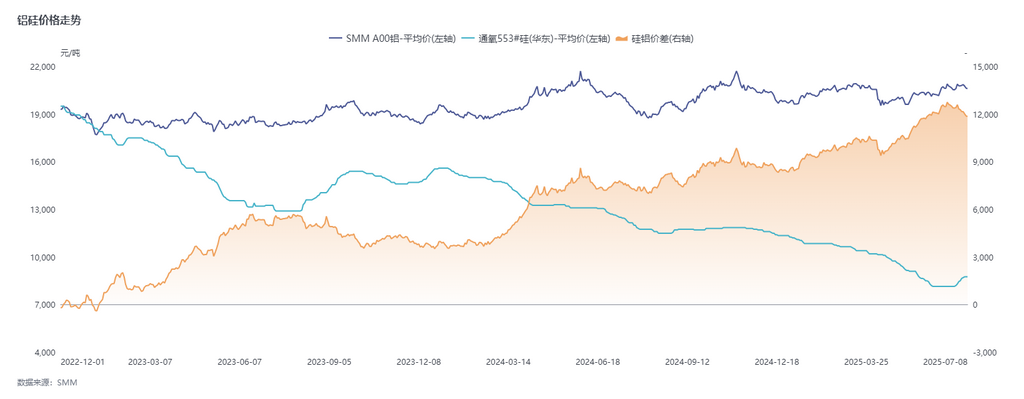

Regarding costs, in June, aluminum scrap prices rose along with aluminum prices. Coupled with the upward movement of core raw material prices such as silicon (oxygen-blown #553 silicon price rose by 600 yuan/mt MoM to 8,750 yuan/mt) and copper, the cost of ADC12 was significantly pushed up. However, the cost pressure was difficult to effectively pass on to product selling prices. Meanwhile, the tightening of raw material circulation increased the difficulty of enterprise procurement, with cost pressure increasing week by week, and the industry's theoretical loss area continued to expand.

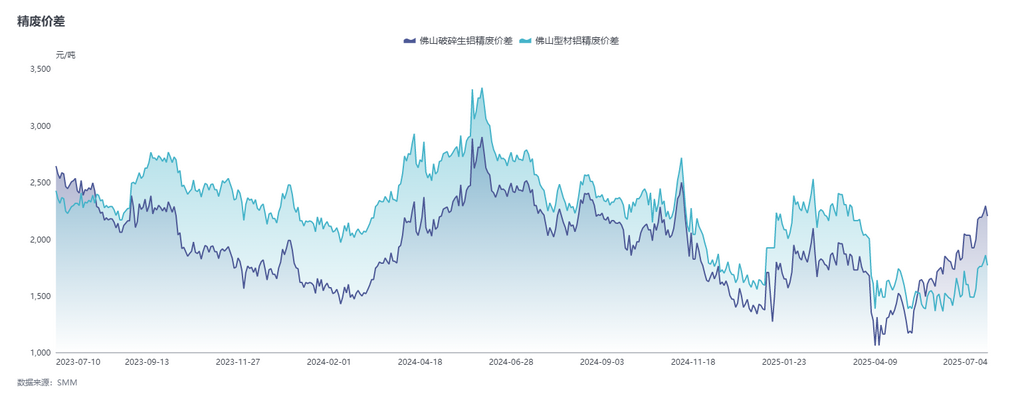

The following chart shows the price difference between A00 aluminum and aluminum scrap:

The following chart shows the price trends of silicon and aluminum:

The following chart shows the average profitability of ADC12 nationwide:

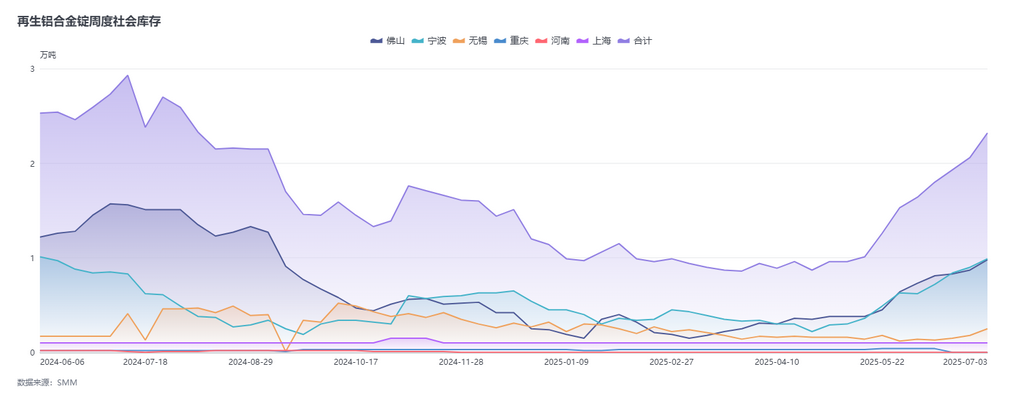

In terms of demand, new energy-related orders performed moderately in June, and the easing of tariff impacts drove a recovery in some downstream orders. However, overall consumption remained weak, and the high aluminum prices continued to suppress downstream purchase willingness. Although the listing of futures increased the inquiry activity of futures-spot traders for delivery brands, the actual consumption support was still insufficient, and the ADC12 price lacked upward momentum. Additionally, social inventory continued to accumulate. According to SMM statistics, the social inventory of secondary aluminum alloy had accumulated for eight consecutive weeks, increasing by 6,866 mt MoM to 23,232 mt at the beginning of July. Against the backdrop of high inventory levels, low-priced goods impacted the market, further intensifying competitive pressure, and the ADC12 price continued to face downward pressure.

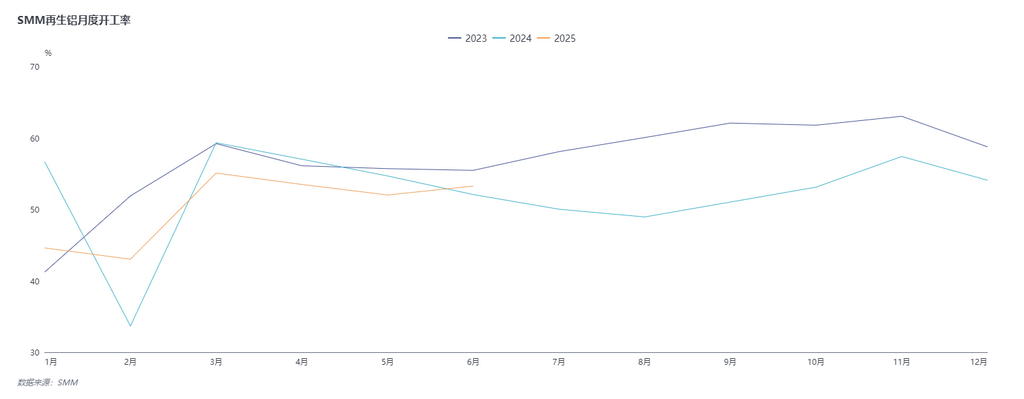

In terms of supply, the operating rate of the secondary aluminum alloy industry increased slightly by 1.25 percentage points MoM to 53.26% in June, up 1.20% YoY. The growth was mainly attributed to two aspects: Firstly, the increase in orders from the NEV sector drove the operating rate of some large factories, mainly producing aluminum liquid, to exceed expectations. Secondly, compared to May, there was no holiday interference in June, and production showed a recovery growth. As July begins, the operating rate trends of secondary aluminum producers continue to diverge. Larger producers, leveraging their stable orders and the advantage of delivery brands, are expected to see an increase in production, driven by the active procurement of ADC12 by futures-spot arbitrage traders. However, the traditional off-season effect continues to manifest, with automakers potentially cutting production plans due to factors such as high-temperature holiday arrangements and finished product inventory backlogs. Additionally, with tightened raw material circulation and intensified cost losses, some producers have already initiated furnace shutdowns for maintenance at the end of June or the beginning of July, which will drag down the overall operating rate of the industry.Overall, it is projected that the operating rate of the secondary aluminum alloy industry will remain stable with a slight decline in July.

Regarding the import of aluminum alloy ingots, according to customs data: In May 2025, the imports of unwrought aluminum alloy stood at 97,000 mt, a year-on-year decrease of 12.1% and a month-on-month increase of 11.8%. From January to May 2025, the cumulative imports reached 464,900 mt, a year-on-year decrease of 11.5%. Compared with April, imports from Malaysia and Thailand declined in May, while Russia, Indonesia, and South Korea were the main contributors to the increase. Notably, Malaysia, as the largest source, saw its share drop below 40% for the first time this year. Currently, overseas quotes for ADC12 have risen by $70/mt from early June to $2,450-2,480/mt, while the import spot price has only increased slightly by 100 yuan/mt to around 19,200 yuan/mt, leading to an expansion of immediate import losses to the range of 600-800 yuan/mt.It is projected that aluminum alloy imports will decline in June and July, with monthly imports continuing to stay below 100,000 mt.

As July progresses, influenced by factors such as reduced aluminum scrap imports and a decline in dismantling volumes due to high temperatures, the shortage of secondary aluminum raw materials is expected to persist, which will continue to support the cost of ADC12. Moreover, the increased difficulty in sourcing materials may further strengthen this support. On the demand side, although market expectations for consumption in the second half of the year have turned optimistic, in the short term, the deepening of the high-temperature off-season in July will continue to suppress the operating rates of downstream die-casting enterprises. Coupled with the high prices of aluminum, which weaken the purchase willingness of terminal orders, the demand slump is unlikely to improve, posing a core resistance to the price increase of ADC12. Overall, the strong cost support and weak demand continue to engage in a tug-of-war, and it is projected that the price of ADC12 will maintain a weak and rangebound pattern in July.In the futures market, the cast aluminum alloy futures are currently in the early stages of listing, with the most-traded contract being the distant-month 2511 futures contract, and the market is in a wait-and-see atmosphere. At this stage, participants are mainly producers, futures-spot arbitrage traders, and traders, with limited participation from downstream enterprises. The futures market has not yet impacted spot prices or altered the current pricing system. In the short term, the trend of cast aluminum alloy futures is expected to continue following that of SHFE aluminum. In the near term, we need to focus on the circulation of raw materials and fluctuations in demand, while continuously tracking the transmission effect on the spot market after the improvement of liquidity in the futures market.

For queries, please contact Lemon Zhao at lemonzhao@smm.cn

For more information on how to access our research reports, please email service.en@smm.cn